European stock markets, led by the Stoxx 600 index, remained relatively stagnant on Monday as the US market observed Labor Day, preventing any substantial momentum. Despite initial gains, European indices like the FTSE 100, DAX, CAC 40, FTSE MIB, and IBEX 35 saw only minor fluctuations. Travel and leisure stocks inched up by 0.5%, buoyed by optimism following a favorable US jobs report, while the European basic resources sector gained 0.6% due to China’s stimulus measures. In currency markets, the US Dollar Index dipped slightly, while ECB President Christine Lagarde’s speech provided no fresh insights. GBP/USD strengthened, and USD/JPY continued to rise, while AUD/USD held steady near its 20-day Simple Moving Average. The Reserve Bank of Australia (RBA) was expected to maintain its key interest rate at 4.1% in Philip Lowe’s final term as governor, and NZD/USD aimed for a sustained recovery. Meanwhile, USD/CAD faced resistance ahead of the Bank of Canada’s upcoming meeting.

Stock Market Updates

On Monday, the US stock market remained closed due to the Labor Day holiday, while European stock markets experienced minimal change, struggling to sustain momentum after initially brushing off recent negativity. The Stoxx 600 index concluded the session nearly unchanged, retreating from earlier gains that had pushed it to its highest level since August 9. Key European indices, including the FTSE 100, DAX, CAC 40, FTSE MIB, and IBEX 35, recorded mixed movements, with minor fluctuations in either direction.

Travel and leisure stocks exhibited a 0.5% gain, reflecting improved sentiment towards equities following the release of the US jobs report the previous Friday. Investors interpreted signs of a potential economic slowdown as a factor that might temper the Federal Reserve’s hawkish stance on interest rates. Additionally, the European basic resources sector recorded a 0.6% increase, partially attributed to China’s announcement of stimulus measures aimed at bolstering its struggling property sector.

In other economic news, German trade data for July indicated a 0.9% month-on-month decline in exports, while imports increased by 1.4%. This data contradicted economists’ expectations of a 1.5% month-on-month decline in exports for Europe’s largest economy, signaling areas of slowdown. During a seminar in London, Christine Lagarde, President of the European Central Bank, emphasized the significance of central banks anchoring their inflation targets, particularly in the context of energy price fluctuations and geopolitical activity.

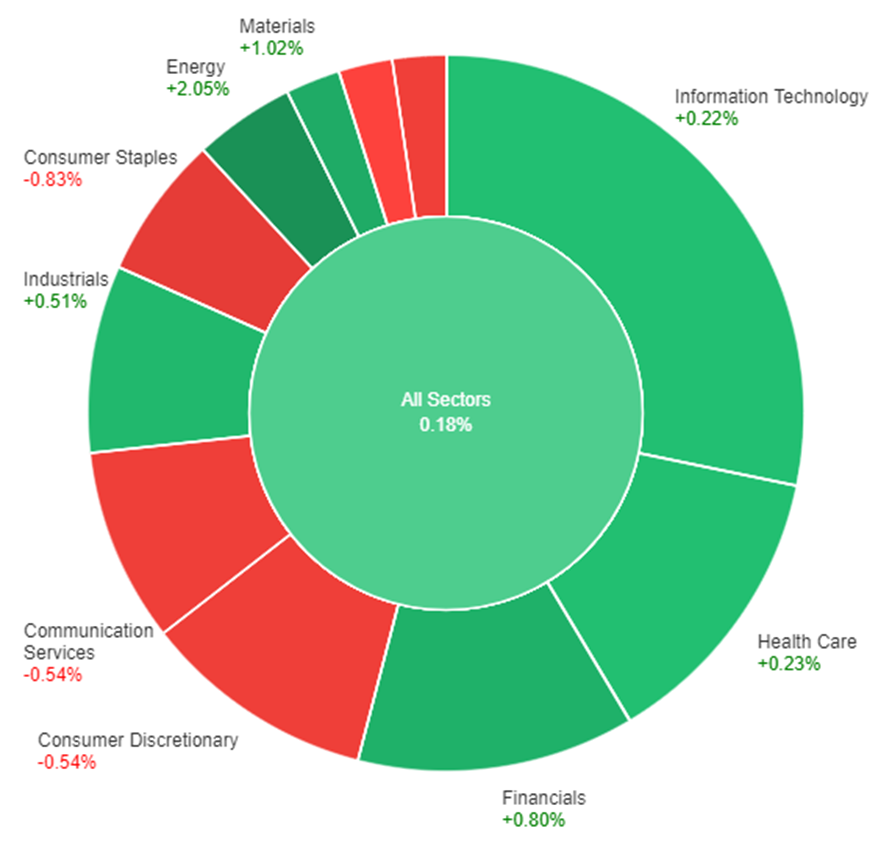

On Friday, the overall market showed a slight gain of 0.18%. The energy sector led the way with a notable increase of 2.05%, followed by materials at 1.02%, and financials at 0.80%. Industrials also saw a modest rise of 0.51%, while health care and information technology sectors had smaller gains of 0.23% and 0.22%, respectively.

In contrast, the real estate sector experienced a slight decline of -0.07%, and utilities and communication services both saw notable decreases of -0.52%. The consumer discretionary and consumer staples sectors both declined by -0.54%, while consumer staples had the largest drop of -0.83%.

Currency Market Updates

In a subdued trading session marked by Wall Street’s closure for Labor Day, the US Dollar Index experienced a slight dip while hovering near 104.00, close to its monthly highs. US stock futures also saw minor declines, and investors awaited the release of July Factory Orders on Tuesday. Meanwhile, European Central Bank (ECB) President Christine Lagarde’s Monday speech offered no new insights, and Eurozone Sentix Investor Confidence continued to deteriorate in September. EUR/USD made a moderate uptick but struggled to hold above 1.0800, maintaining a bearish bias with support at 1.0760. Tuesday’s agenda includes another speech by Lagarde, the release of the August Producer Price Index by Eurostat, and the final Service PMIs.

In currency markets, GBP/USD showed strength, climbing from below 1.2600 to approximately 1.2630, outperforming its peers as EUR/GBP dropped below 0.8550. The UK’s final Service PMI is expected on Tuesday. USD/JPY extended its ascent to around 146.50, potentially reinforcing its bullish outlook if consolidation above that level occurs. AUD/USD closed near the 20-day Simple Moving Average (SMA) around 0.6460, recording modest gains against a weakening US Dollar. The Reserve Bank of Australia (RBA) is set to announce its monetary policy decision on Tuesday, with the consensus anticipating the maintenance of the key interest rate at 4.1%. This meeting marks the last one with Philip Lowe serving as governor of the RBA. NZD/USD remained relatively flat, with critical support at 0.5900 and trading below the 20-day SMA at 0.5970. To establish a more enduring recovery, the Kiwi needs to secure a daily close above 0.6000. Finally, USD/CAD held onto its Friday gains but faced resistance around 1.3600, with the Bank of Canada’s monetary policy meeting scheduled for Wednesday.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USDSees Modest Uptick Amid ECB’s Inaction, Eyes on Eurozone Data and US Factory Orders

The EUR/USD currency pair saw a slight increase in value on Monday, rebounding from a recent two-month low. Although it remained above 1.0770, it struggled to establish firm support above 1.0800. European Central Bank (ECB) President Christine Lagarde’s comments on central banks’ role in managing inflation expectations had little impact on the market. Upcoming events include the final Eurozone Services PMI reading and Eurostat’s Producer Price Index release, while the US Dollar experienced a minor decline ahead of the release of Factory Orders data.

According to technical analysis, the EUR/USD dropped a bit on Monday and is currently trading sideways between the lower and middle bands of the Bollinger Bands. This movement suggests the possibility of another downward move to reach the lower band. The Relative Strength Index (RSI) is currently at 39, indicating that the EUR/USD is trending lower and attempting to stay in a bearish trend.

Resistance: 1.0832, 1.0880

Support: 1.0780, 1.0734

XAU/USD (4 Hours)

XAU/USD Surges to Four-Week High as USD Weakens Amid Fed Uncertainty

The US Dollar continued its decline in the forex market, driving XAU/USD to a four-week high at $1,949.02 per troy ounce. This decline was triggered by disappointing US macroeconomic data, which raised doubts about the Federal Reserve’s tightening policies. The August ADP Survey revealed a slowdown in private job creation, and Q2 GDP figures were downwardly revised. Despite this, July Pending Home Sales exceeded expectations. Stock markets saw modest gains, and government bond yields retreated as the probability of the Fed keeping rates on hold next September increased to 88.5%, according to the CME FedWatch Tool. However, concerns arose about the Fed pressuring regional lenders to bolster their liquidity strategy, causing Wall Street to retract from recent highs. The upcoming focus is on US inflation data, specifically the July Core PCE Price Index, which is expected to show a slight easing in August. Lower inflationary pressures may reinforce the case for no further rate hikes and boost investor sentiment.

According to technical analysis, XAU/USD traded flat on Monday and formed narrow Bollinger Bands. At present, the price is close to the lower band, indicating a possibility of a slight increase in Gold’s value, but it’s still in a consolidation phase. The Relative Strength Index (RSI) currently stands at 50, suggesting that the XAU/USD pair is now in a neutral position.